Poultry Farm Business Loan in India

Personal loan starting

@ 11.50% p.a

All you need to know

Personal loan for all your needs

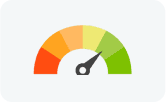

Check Your Credit Score

Higher credit score increases the chances of loan approval. Check your CIBIL score today and get free insights on how to be credit-worthy.

Check Credit Score

Home Extension Loan Affordable Housing Loan PMAYQuick Cash Plot & Construction Loan Balance Transfer Home Loan Top Up Home Loan EMI Calculator PMAY Calculator Balance Transfer & Top-up Calculator Home Loan Eligibility Calculator Area Conversion Calculator Stamp Duty CalculatorKnow MoreCheck Credit Score Home Loan Rates & Charges Home Loan Documents Required Home Loan Online RERA Approved Housing Projects

Business Loan EMI Calculator Business Loan Pre-payment Calculator GST Calculator Foreclosure Calculator Hybrid Term Loan Machinery Loan MSME Loan Small Business LoanBusiness Loan Rates & Charges Business Loan Documents Required

Used Car Loan Loan On Used Car New Car Loan Two Wheeler Loan Used Car EMI Calculator Two Wheeler EMI Calculator Apply Now Apply Now

Know More Apply Now Loan Against Securities Rates & Charges Loan Against Securities Documents Required Loan against Shares Loan against mutual funds Check Credit ScoreLoan Against Securities Rates & Charges Loan Against Securities Documents Required

Know More Apply Now Loan Against Property Rates & Charges Loan Against Property Documents Required EMI Options Hybrid Term Loan Secured BL (SBL) Loan Against Property EMI Calculator

Know More Apply Now Education Loan Rates & Charges Education Loan Documents Required Education Loan EMI Calculator Request a Callback

Sign in to unlock

special offers!

Setting up a poultry farm can be a lucrative business idea. However, it requires significant investment in infrastructure, livestock, feed, and other essentials. With a loan for poultry farm, you can receive the financial support to establish and grow your business conveniently. It is a secure and hassle-free way of securing the required funds without dipping into your savings.

Starting a poultry farm requires proper planning and adequate funding. Understanding the eligibility criteria for a poultry farm Business Loan in India can help applicants prepare more effectively and improve their chances of approval. Lenders assess financial stability, business viability, and repayment capacity before sanctioning the loan.

Meeting these criteria can improve the likelihood of securing a poultry farm Business Loan smoothly and efficiently.

Starting a poultry farm requires adequate capital investment which can be challenging to arrange without the help of a business loan. Lenders typically ask for a set of documents from applicants to evaluate loan eligibility and assess risk. Some key documents required include:

Business Profile and Plan

A comprehensive business plan is important to convince lenders about the viability and profitability of your proposed poultry farming venture. The plan should include details about infrastructure, location, types of poultry birds, projected costs and revenues, marketing strategy etc.

Financial Statements

Share the financial projections for the next 3-5 years in the form of a profit and loss statement and cash flow statement. This helps analyze the expected profitability and loan repayment capacity.

Collateral Details

Since agricultural loans are considered high risk, lenders ask for collateral security against the loan amount. Common assets provided include agricultural land, machinery, vehicles etc. You can check loan eligibility.

Most poultry farm loans range between Rs. 10 lakh to Rs. 1 crore based on the scale of operations. The interest rate charged is slightly higher than general business loan since it's an agricultural venture. Interest is usually in the range of 12.5-14% per annum.

The maximum repayment period granted is 5-7 years depending on the lender. EMIs are calculated on the reducing balance method to help lower monthly payments. You can check sample loan EMIs

Several government initiatives support loans for poultry farming in India to encourage rural entrepreneurship and livestock development. Subsidy programs may be available under central or state-level schemes, subject to eligibility norms and category-specific limits.

Under certain agricultural and allied activity programs, borrowers may receive capital subsidy benefits linked to infrastructure development, equipment purchase, or expansion. Applicants should verify the scheme guidelines before applying for a poultry farm Business Loan in India.

Financial institutions may also extend credit under priority-sector lending norms, where applicable. However, subsidy availability, amount, and conditions vary by region and scheme.

Before applying for a chicken farm Business Loan, borrowers should review the latest notifications from relevant authorities and confirm whether the poultry farm business plan qualifies for government assistance.

Broiler and layer poultry farming have different business models, cost structures, and income cycles. As a result, loan requirements and repayment patterns may vary. The table below highlights the key differences between broiler and layer poultry farming loans.

| Basis | Broiler Poultry Farming Loan | Layer Poultry Farming Loan |

|---|---|---|

| Purpose | For raising chickens for meat production. | For raising hens for egg production. |

| Loan Tenure | Usually short- to medium-term due to the rapid growth cycle. | Often, a longer tenure is required as egg production continues. |

| Working Capital Needs | Higher recurring cost for feed and chicks in short cycles. | Ongoing expenses for feed, maintenance, and healthcare. |

| Income Pattern | Lump sum income after each batch sale. | Regular income from continuous egg sales. |

| Repayment Structure | Structured around batch sales and quick turnover. | Aligned with steady monthly cash flow from eggs. |

Understanding these differences helps borrowers choose the right poultry farming loan based on their business model and financial goals.

Some lending institutions may offer a poultry farm loan without collateral, particularly for smaller ticket sizes or under specific schemes. However, approval depends on credit profile, business viability, and applicable lending norms.

Under certain government-backed or priority-sector programs, collateral-free limits may apply. Applicants seeking a poultry farm Business Loan in India without security must demonstrate stable projected cash flows and a well-prepared poultry farm business plan.

Eligibility for unsecured options varies by lender policy. Borrowers should carefully review terms and understand that interest rates and loan limits may differ for collateral-free facilities.

While banks like SBI, Punjab National Bank provide agricultural loans, it's best to approach lenders specialized in this space:

NABARD: Offers refinance support to RRBs and co-operative banks. Interest rate starts at 7%.

SIDBI: Has dedicated lending schemes for poultry and other animal husbandry related ventures.

Food Corporation of India: Finances projects larger than Rs. 50 lakh in scale. Rate of interest 10.25-11.25%.

You can compare loan terms offered by different lenders on their websites or by visiting their branches locally. Make sure to check loan processing times as well.

To start a poultry farm, you can consider securing finances from lenders that specialise in this space like:

Follow these steps to get a loan for a poultry farm:

Yes, you can get a loan on a poultry farm under 'loan against agricultural land.'

Lenders typically offer loans for poultry farming ranging from Rs. 10 lakh to Rs. 1 crore. For a more accurate amount, please visit the official website of your preferred lender.

Yes, since agricultural loans are high-risk, lenders may ask for collateral. However, this requirement varies from lender to lender. Please check the official website of your preferred lender to determine the collateral requirements.

Submitted successfully

Uh oh, something went wrong

Please try again later.

Start an SIP in minutes by signing up with the Tata Capital Moneyfy App. We are your one stop shop for all things investment.

SMS sent successfully!

SMS sent successfully!

An SMS has been sent to XXXXXXX051

Click on the link in the message to download the Moneyfy App.

Looking for a seamless loan experience? Get the Tata Capital Loan App and Apply for loans, Download Account Statement/Certificates, Track your requests & much more.

SMS sent successfully!

An SMS has been sent to XXXXXXX051

Click on the link in the message to download the Moneyfy App.

Thank you for subscribing

We will send news and updates to your registered email ID

Trust the links that start from https://www.tatacapital.com

Do not make payments in any individual’s bank accounts.

Call our Customer Care Number 1860 267 6060 for assistance

For any assistance, contact our customer support

rahul.sharma@gmail.com

SMS sent successfully

SMS sent successfully